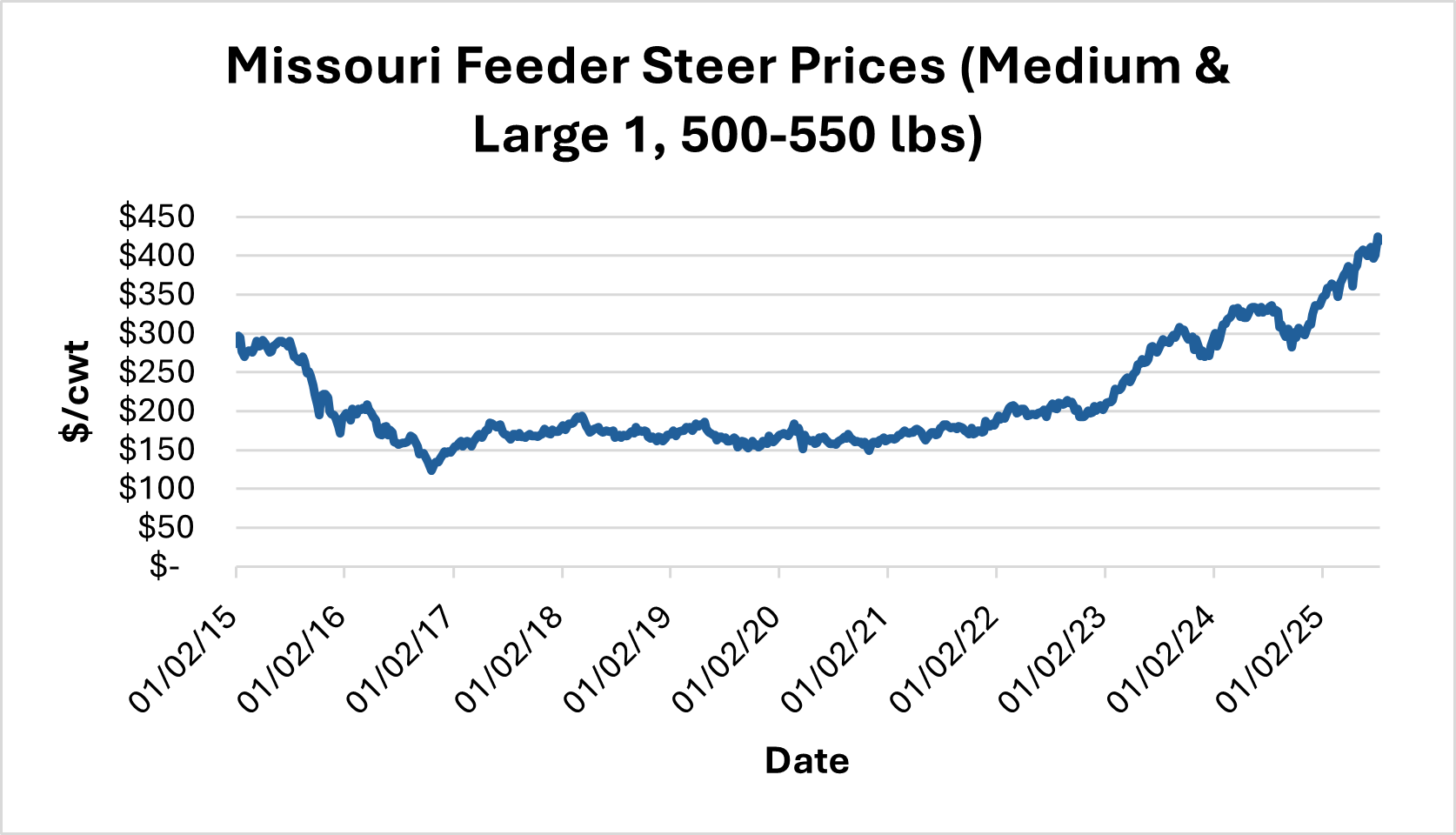

Mo. Forsyth. There are still no indicators that the rising cost of livestock will slow down. The USDA Livestock, Poultry & Grain Market News report shows that Missouri feeder steer prices have been rising since 2015.

According to a press release from Jacob Hefley, an agricultural business specialist with the University of Missouri Extension, high prices usually translate into higher profitability, which is excellent news for cattle producers. But this also means a bigger tax payment, which is something most producers would prefer not to consider.

According to Hefley, there are some tax changes to be aware of that could have an impact on planning now that the 2025 budget reconciliation bill, also known as the One Big Beautiful Bill Act, has been signed into law.

Permanent bonus depreciation

Producers can deduct a portion of asset costs in the year that the assets are put into operation thanks to bonus depreciation. 100% bonus depreciation was introduced by the 2017 Tax Cuts and Jobs Act (TCJA) and has been phased out over time. The first plan was to cap the 2025 level at 40% and phase it out completely by 2027. However, for property purchased after January 19, 2025, 100% bonus depreciation is permanently permitted under the 2025 budget reconciliation bill. Bonus depreciation can be used by producers that expect big earnings this year and in the future to offset income and lower their tax liability. It is crucial to remember that unless a taxpayer chooses to opt out, bonus depreciation is applied automatically.

Increased expensing limitations under Section 179

Section 179 permits producers to expense the entire cost of eligible asset purchases in the year of their placement in service, much like bonus depreciation does. Section 179, however, has restrictions and needs to be elected. The yearly Section 179 deduction cap was raised from $1.22 million for the 2024 tax year to $2.5 million under the new law. Furthermore, the investment cap has been raised from $3.05 million to $4 million, which is the highest amount of property that can be taken into consideration. This implies that the deduction is lowered dollar for dollar by the excess amount if more than $4 million in qualified property is put into operation in a single year. According to Hefley, after 2025, the investment and deduction maximum amounts would be adjusted for inflation. Although many producers might not be impacted by these levels, major operations or years with exceptionally high asset purchases may be impacted by the higher restrictions.

Indefinite extension of the Section 199A deduction

The extension of the Section 199A Qualified Business Income deduction is another significant development. Section 199A, which was established by the TCJA, permits owners of pass-through companies, including partnerships, LLCs, and sole proprietorships, to deduct up to 20% of their eligible business income from their federal tax returns. This deduction, which was initially scheduled to cease in 2025, has now been extended indefinitely. According to Hefley, this might continue to reduce your personal taxes for years to come if you qualify, which many producers do.

He notes that only a portion of the new policy changes that could impact you are covered by the tax provisions listed above. Depending on your business, additional regulations and restrictions may apply even within the previously covered topics of bonus depreciation, Section 179, and Section 199A. The optimum tax plan for you may also be impacted by a number of variables, including changes in output, market trends, and input cost fluctuations. To find out how the new law can affect your farm, consult with a knowledgeable tax advisor.

Visit https://muext.us/AgBizPeople to locate the local MU Extension agriculture business specialist for additional information.